Dexcom Stock: How Much Growth is Left?

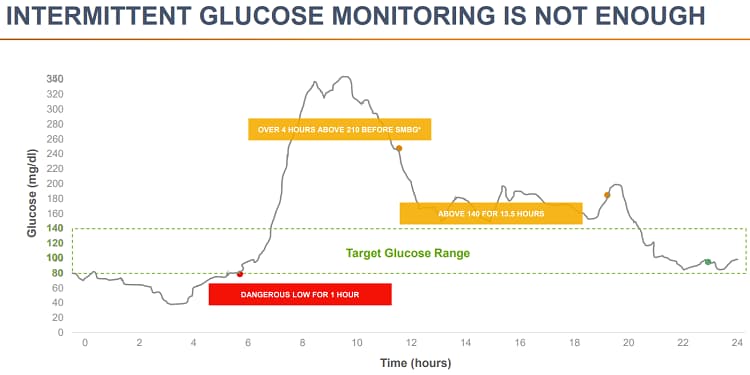

“I never realized that I loved hiking,” says a moderately attractive woman named Abby who breaks into tears over the thought of her newly found hobby. This woman has clearly never encountered a tick in her life, but if she did, the tick probably wouldn’t find her blood to be that tasty. You see, Nancy has diabetes, and for whatever reason, she couldn’t go hiking before she found out about Dexcom (DXCM). For diabetics like Abby, Dexcom’s device allows for an unprecedented look into blood sugar (glucose) levels, the bane of every diabetic. In the below chart you can see three dots – the typical intermittent testing with finger pricks – while the solid line shows the Dexcom device continuously measuring blood sugar.

The last time we looked at Dexcom was two years ago in a piece titled A Large-Cap Diabetes Stock That’s Growing Like Mad. In both our tech stock report and tech stock catalog, we’ve listed Dexcom as a “like” noting that – as of several years ago – they appeared to have plenty of growth and opportunity ahea