Challenges Ahead for Twist Bioscience Stock

There’s always a delicate balance between being too hands on with a stock and not paying close enough attention to how its business evolves. Revenue growth is the one metric that cuts through all the noise and distills it down to what’s most important for a disruptive technology stock. Is a company able to monetize their technology and capture market share in a large total addressable market (TAM)?

In addition to monitoring revenue growth, it’s good to have an elevator pitch that quickly articulates your bull thesis. For example, Twist Bioscience Corporation (TWST) is a company that produces synthetic DNA strands on demand for their clients. The need for this service has expanded significantly with the emergence of synthetic biology. Therefore, Twist Bioscience is a pick-and-shovel play on synthetic biology tools that should grow along with the entire synbio industry. Indeed, we see this to be the case over time.

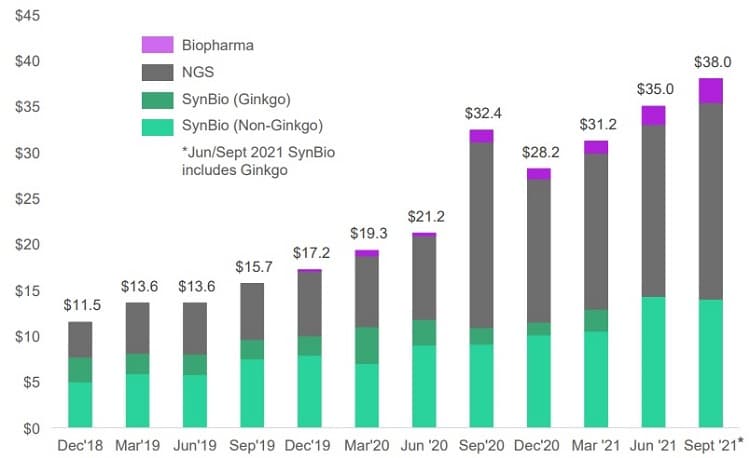

Aside from showing consistent quarterly revenue growth over the past three years, this chart contains other useful insights. Notice how they recently stopped breaking out revenues for